Amazon (AMZN) represents the present and future profile of the broader online retail industry. But more than that, under founder, chairman and CEO Jeff Bezos, it reflects a new innovatively growth-oriented American company that’s blazing a trail of efficiency and expansion that cuts across many industries. Started in 1995 as the “Earth’s biggest bookstore,” by 2013 it posted annual sales of $74.4 billion. But by 2016, revenues had leaped to $135.9 billion. This year, analysts project sales to advance 30 percent — yes, 30 percent, and 29 percent more in 2019.

Its stock has been an admirable performer, climbing from a low of $36 a share in 2007 to $1,305 as of Jan. 16, 2018. Equity analyst Tuna Amobi of CFRA has a price target of $1,350, “based on a price-to-sales of 2.9 times our 2019 estimate, a relatively modest discount to the medium multiple for the internet retail peer group, and slightly above Amazon’s recent historical averages.”

Amobi also sees “further market share gains versus tradition retailers in Amazon’s core electronics and general merchandise offerings, thanks to a focus on providing value to consumers through selection, price and convenience.”

Receive News & Ratings Via Email – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings with MarketBeat.com’s FREE daily email newsletter.

Last week JPMorgan raised its price target for Amazon to $1,385 a share from $1,375, with a rating on it of “overweight.”

Amazon.Com: One Of The Best Picks For 2018-2028

Summary

Investors and models that focus on near-term market multiples fail to appreciate the long-term growth prospects of companies like Amazon.com.

Since 2011, Amazon’s R&D spending has increased 8x while revenue has increased 3x and adjusted operating profit by 5x. Increased investments in R&D should continue to help drive cash flows.

The tremendous growth potential of Amazon was erroneously ignored by those who focused on near-term earnings and market multiples.

AMZN is Citi’s top Internet pick for 2018.

While we do not share Citi’s view, because of the company’s flattening ROIC profile in 2018, we do think it deserves consideration as the top Internet pick for 2018-2028.

On January 5, 2018 Citi named Amazon.com (AMZN) its top Internet pick for 2018 and raised its price target for the stock to $1,400 from $1,250. The analyst based his recommendation on expectations for 30% sales growth, margin expansion, and an attractive current valuation.

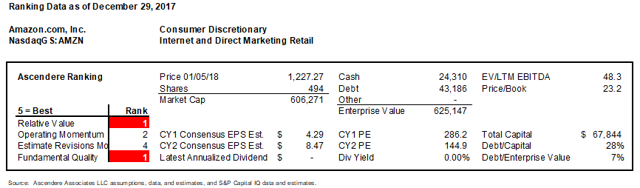

Poor relative ranking on a quantitative model, but still a great stock idea. Why?

Amazon.com ranks poorly on our quantitative ranking model, yet Citi has named it its top pick. Who is wrong, and why?

This is the wrong question to ask. It is better to ask what is the analyst telling us? What is the model telling us?

Citi’s view on Amazon.com

Citi cites revenue growth, margin expansion, and valuation. With AMZN trading at 200x NTM EPS, obviously Citi is citing some forward multiple several years out and some multiple not based on EPS. This makes sense given the 24-27% annual revenue growth and gross margin expansion over the last few quarters.

The consensus 2021 EBITDA estimate for AMZN is $59,483m, up from $18,976m for 2017, at a 33% compound growth rate. That represents a much more acceptable 10.1x multiple. The company’s long history of expansive growth lends credibility that this EBITDA target is achievable. This must be the source of the “compelling valuation” the analyst is citing.

A simple quantitative model’s view on Amazon.com

Today, the stock ranks poorly on valuation, and the company is ranked poorly for operating momentum and fundamental quality, yet consensus estimate revisions are relatively high. This is largely due to the impact of the Whole Foods acquisition, which should simultaneously depress ROIC and drive estimates higher in the short term.

Exceptions to every rule

There are exceptions to every rule. The Citi analyst is looking ahead and analyzing what matters most to Amazon.com – growth prospects several years out. In our contrast, our model uses trailing multiples, changes in capital efficiency ratios, and short-term changes in estimate revisions to measure the relative attractiveness of stocks.

The advantages and limitations of the model are the same – its consistency and the assumption that recent trends are likely to persist. It has tended to work well on average over time.

As long as we keep in mind the advantages and limitations of the ranking model, we can use it effectively to selectively override the quantitative rankings.

Short-term metrics do not capture exceptional growth potential

In April 2011, when the stock was priced at $186, investors were frustrated with Amazon.com and were focused on near-term earnings reports rather than on its free cash flow potential.

As I explained in that April 2011 note, the ranking model did not capture the entire story of Amazon:

“Any company that can double R&D spending and still grow reported margins deserves to be studied closely regardless of valuation. The incremental spend on R&D should be viewed as an investment in future cash flows as opposed to an expense.”

Amazon’s earnings angst inexplicably persisted through at least 2014

Perhaps the best example of this widespread investor angst with Amazon’s earnings was captured from an October 2014 discussion on CNBC between CEO Ari Zoldan of Quantum Networks and an unnamed manager, presumably of the Olstein Funds, on whether a $100 stock price target for AMZN stock was justified versus the $289 price at that time.

Zoldan pointed to the long-term growth prospects of the company while the analyst argued that AMZN’s stock was trading too high on “real world” multiples.

What the manager and so many others failed to understand at the time was that AMZN’s near-term earnings were artificially depressed in part by high R&D spending, which in turn should have been assumed to be an investment in future cash flows.

Future free cash flow expectations define value, not multiples

Future free cash flow expectations discounted at a company’s cost of capital to a present value – not some near-term market multiple – determine a stock’s value. Market multiples are just rules of thumb for what the present value of future free cash flow might be, so at times relying solely on multiple analysis can be misleading.

Since 2011, Amazon’s R&D spending has increased 8x while revenue has increased 3x and adjusted operating profit has increased 5x

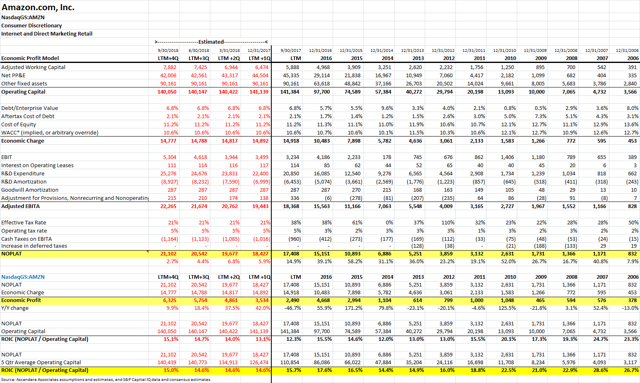

Since 2011, the company’s R&D spending has increased 8 times! This has helped it drive revenue higher by 3 times. Early R&D components such as Amazon Web Services (AWS) are now a key driver of the company’s future growth prospects.

In 2011, R&D spend excluding stock-based compensation was $2,617m, representing 5.4% of net sales of $48,077m. This was up from 4.3% of R&D as a percentage of sales in 2009. Today, LTM R&D spending of $20,850m represented 12.9% of $161,154m of net sales. Amazon.com’s free cash flow prospects continue to expand in part due to its ongoing increases in R&D.

In the 10-year ROIC model below, we can see that Amazon is efficiently managing its assets to drive its operating profit above its cost of capital. Net operating profit less adjusted taxes (NOPLAT) has increased nearly 5x since 2011 while its economic profit has increased nearly 2.5x. ROIC has declined to 15.7% from 18.8% in 2011, with growth of NOPLAT not keeping up with the growth of the operating capital used to drive those profits. This decline in ROIC is probably what drove the decision to acquire Whole Foods.

In our opinion, Amazon is not the best Internet stock pick for 2018

The flat ROIC indicates multiple expansion (on some far out projection like 2021 EBITDA) is unlikely in the near term. This model also lends credibility to any 10-year DCF model. It shows the company has a long track record of efficiently managing and growing its business, thereby supporting high long-term cash flow growth assumptions for the company.

Because other companies may demonstrate expectations for both free cash flow growth and ROIC expansion, Amazon does not deserve to be the number one choice for 2018, in my opinion. As for choosing the top Internet pick for the next 10 years, I do think AMZN would be a solid contender given its impressive track record of managing its R&D and other aspects of its business for long-term growth potential.

Risks

Buying stocks entails high risk, including the risk of 100% loss. Short selling stocks entails higher risk than buying stocks. In theory, potential short sale losses are infinite, indicating that an investor could lose multiples of their initial short sale investment. Please read about some key risks associated with the model portfolio strategies and associated equity research, as well as our disclosures and disclaimers below and on our welcome note.